AlcancIA

Agente IA que crea wallets Web3 invisibles, propone metas de ahorro, conecta amigos y usa DeFi con stablecoins. Usa ElizaOS, Astar y Hyperlane para facilidad e interoperabilidad.

- 0 Raised

- 869 Views

- 0 Judges

Tags

Gallery

Description

Develop an AI agent that allows users to invisibly create Web3 wallets, set personalized savings goals, and form savings groups with friends. Funds will be managed through low-risk DeFi strategies using stablecoins, with incentives and penalties based on savings consistency. Technologies such as ElizaOS, Astar, and Hyperlane will be used to enhance user experience and enable cross-chain interoperability.

Objectives

Promote the habit of saving among individuals unfamiliar with blockchain by using an AI agent that helps them define and maintain personalized financial goals within a mutual support group.

Business Goals

• Web3 Adoption: Make it easy for non-technical users to enter the Web3 ecosystem through a simplified user experience.

• Encourage Saving: Promote saving habits in Mexico through accessible and collaborative digital tools via Telegram (or WhatsApp).

• Hackathon Participation: Integrate sponsor technologies (Hyperlane, MXNB (Bitso), Chipipay) to compete in the relevant tracks.

• Non-prioritized: Mantle and Soneium.

User Goals

• Interact with the blockchain using wallet addresses and assist in wallet creation without requiring prior knowledge.

• Set personalized savings goals (amount, duration, frequency).

• Form savings groups with friends and track collective progress.

• Receive incentives for maintaining savings consistency.

• Access financial tips and personalized reminders.

Non-Goals

• Implement MXN-to-crypto on/off ramp in this phase (to be simulated for the demo).

• Develop a full mobile or web application (the focus will be on Telegram).

• Support for multiple languages (Spanish will be the focus for the demo).

Product Triangle

Audience

• People with a bank account.

• Telegram or WhatsApp users.

• 18+ years old.

• Individuals who want to save but don’t know how to start.

• Not crypto or blockchain experts.

What problem does it solve, and why now?

• Informal and inefficient saving practices.

• Lack of accessible tools for financial goal setting.

• Weak financial education.

• Blockchain is powerful but largely inaccessible.

• Telegram and AI can bridge both worlds.

What WILL it do?

• Create wallets for on/off ramp interaction without technical knowledge.

• Define personalized savings strategies using AI.

• Enable users to form savings groups with friends.

• Incentivize consistency through variable yields.

• Penalize missed contributions via interest redistribution.

• Provide clear visualization of savings and progress.

• Simulate SPEI for the demo.

What will it NOT do?

• Offer complex or high-risk yields.

• Act as a wallet, bank, or traditional savings group (“tanda”).

• Allow direct user interaction with DeFi protocols.

• Display other users’ information.

• Include full web or mobile interfaces.

What WILL it be?

• An AI agent on Telegram (WhatsApp in the future).

• An open-source app focused on community saving.

• A yield generator using stablecoins.

• A tool for financial education and habit-building, not traditional finance.

What will it NOT be?

• A provider of regulated financial services.

• A social network.

• A replacement for traditional banking tools.

• A platform for trading or speculative investments.

• A wallet.

KPIs (How We Measure Success)

• Number of savings groups created.

• Percentage of users meeting their weekly goal.

• Number of savings cycles completed per user.

• MAUs and 30/60/90-day retention.

• Failure vs. success rate per week.

• Percentage of users coming from informal saving methods (tanda, piggy bank, etc.).

• Successful referrals (viral loop on Telegram/WhatsApp).

User Stories

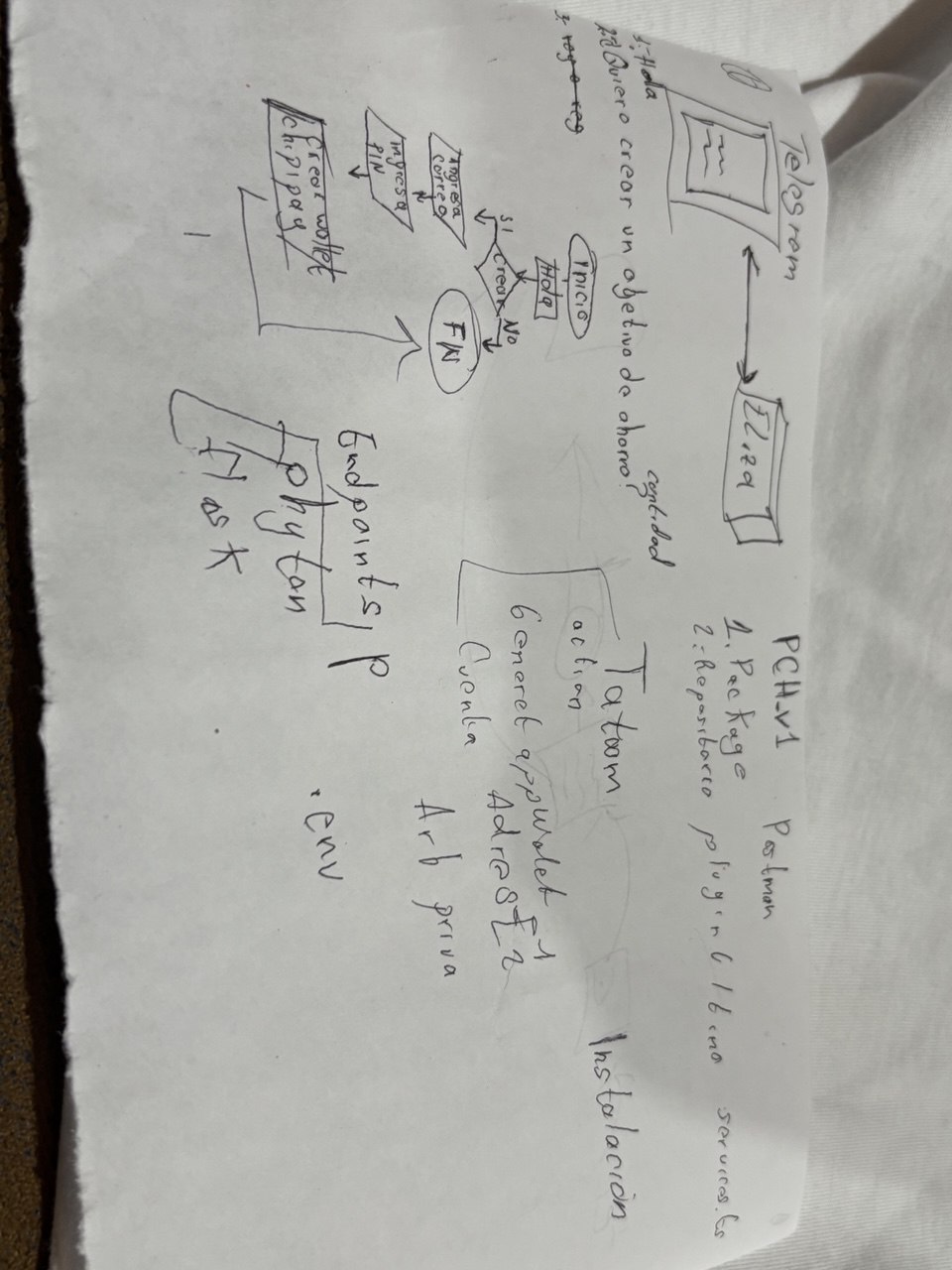

1. Strategy Creation: As a new user, I want to create a strategy linked to a wallet address, with assistance in creating a Web3 wallet effortlessly so I can start saving.

2. Set a Savings Goal: As a user, I want to define my savings goal by specifying the amount, duration, and frequency.

3. Form a Savings Group: As a user, I want to invite friends to join a savings group so we can motivate each other.

4. Make Contributions: Make deposits to meet your savings goal.

5. Track Progress: As a user, I want to see my own progress and my group’s progress to stay motivated.

6. Receive Incentives: As a consistent user, I want to earn rewards for making my periodic contributions.

7. Get Reminders: As a user, I want to receive notifications reminding me to make my contributions and offering financial tips.

Technical Considerations

• ElizaOS: A framework for building the Telegram agent, enabling personalized interactions and state management.

• Hyperlane (Eigen Layer): Enables interoperability between Arbitrum and Soneium, allowing asset and message transfers across chains.

• DeFi Vaults: Implementation of low-risk stablecoin strategies to generate yield on the collective savings group funds.

• On/Off Ramp Simulation: For the demo, MXN-to-crypto conversion will be simulated via hardcoding, with no actual SPEI integration.

Chains to be used:

• StarkNet

• Arbitrum

• Soneium

Assets to be used:

• ASTR

How Does the Penalty System Work?

Goal: Gamify consistency and generate positive social pressure.

Mechanics

1. Weekly → Checkpoint

• The AI agent verifies whether the user made their contribution.

• If not, the user is marked as “failed.”

2. Penalty for Failing

• The user loses the right to earn interest for that week.

• Bonus: their share of the interest is redistributed among those who did contribute.

• This encourages:

• Active participation.

• Light social pressure (without shaming).

• Greater rewards for consistent users.

3. Recovery

• If a user fails 3 times in a row, they are removed from the savings group, with the option to withdraw their funds.

Github Link:

https://github.com/robz323/ethcdm-alcancIA.git

Video:

https://drive.google.com/file/d/1Iodg3RHRERgYG6VP3OVLLjvYNdcx8wES/view?usp=sharing